Lessons from a Volatile Seasonality Trade

On rebalancing even when it feels wrong

In RW Pro, we’ve been trading a seasonal play on natural gas that’s provided some valuable lessons in managing short, volatile positions.

The trade is simple: short natural gas futures around the winter months. I like to express it as a short position in BOIL, the 2x leveraged natural gas ETF.

It’s a seasonality play, but you also get exposed to a nice basis decay tailwind. Natural gas futures curves are usually steep, and the front months, which BOIL is most exposed to, tend to deliver consistent roll-down. You also get exposed to the frictions of a leveraged ETF: tracking error, volatility drag. All working in your favour when you’re short.

It’s a simple, dumb edge. It doesn’t shoot the lights out on its own, but it’s a nice little kicker to a broader portfolio. Typical of the stuff we trade with the RW Pro group.

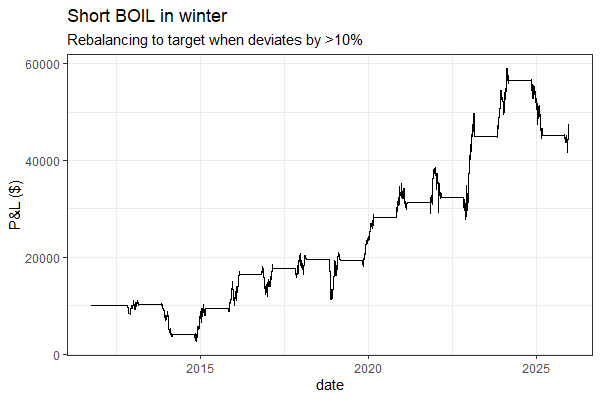

If you backtest it, you’ll see it’s made money in a very ugly, uncomfortable way.

CAGR is about 12%, Sharpe is around 0.5. Certainly nothing to write home about, but a decent enough diversifier.

The thing to note is that it’s volatile as hell. It’s gone at about 50% annualised volatility, and it’s only in the market for four months a year!

This Year’s Ride

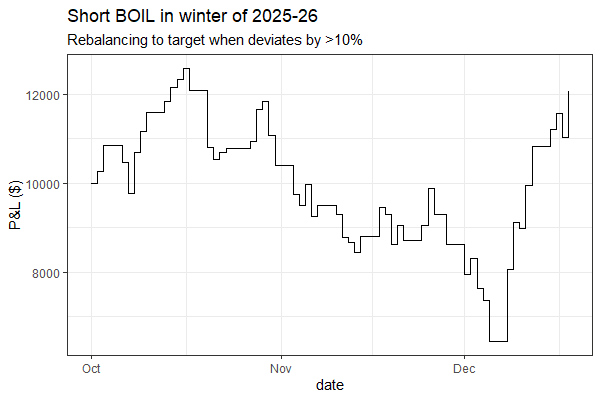

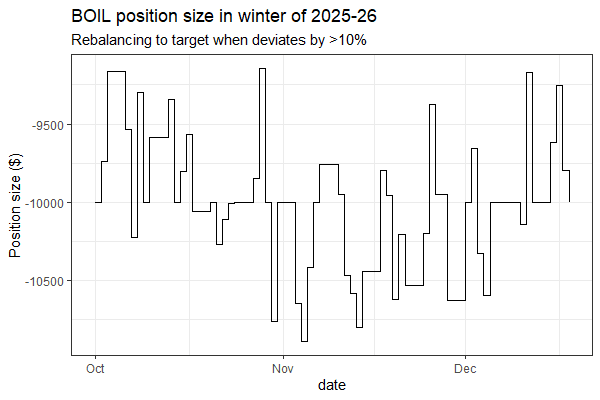

Here’s what the trade looks like so far this year, maintaining a roughly constant dollar exposure (rebalancing if it drifts from target):

You can see it was bleeding cash for a while before recently turning positive.

But the P&L isn’t the main point here. The volatility is.

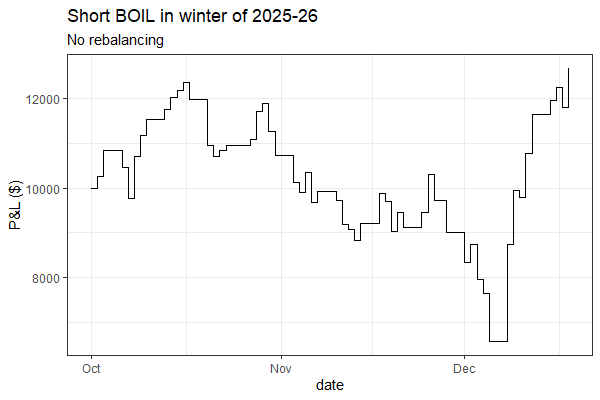

How does it look if you don’t rebalance? Here’s the P&L:

It’s actually made a little more than if you did rebalance - but that’s not a reason to avoid rebalancing.

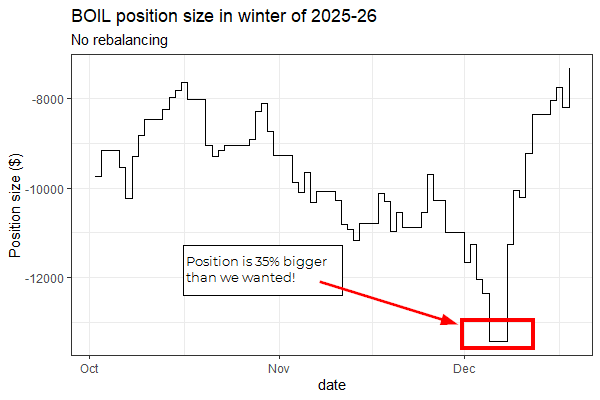

When you were at maximum drawdown without rebalancing, you were sized way larger than you intended.

Here’s the position size over time if you didn’t rebalance:

If we didn’t rebalance, we got lucky that the trade turned around the next day and made a lot of money.

But it could just as easily have been down by that amount again. No matter how crazy things get, they can always get crazier.

And how would you feel in that position at that time?

You’re sized way bigger than you ever intended (about 35% bigger), you’ve already bled a ton of cash, and now you’re facing the prospect of even more losses.

On the other hand, here’s the position size over time with rebalancing:

Totally different risk profile, totally different emotional state! Practically same P&L. And we never let the position get out of hand.

This is the job rebalancing does. It keeps your risk budget constant.

You’re saying: “I want X dollars of seasonal/decay edge, and I’m willing to accept Y units of nat gas volatility to get it.”

Without rebalancing, you’re letting the market decide how much risk you’re taking.

And you wouldn’t want the market dictating the size of your short position in one of the most volatile assets out there.

A sustained rally - cold snap, supply disruption - literally turns a sensible position into an existential one.

Why This Might Feel Wrong

When you rebalance a short position like this, by definition, you’ll be covering after it goes against you and adding after it goes your way.

That’s going to feel very wrong if you think there’s a difference between realised and unrealised losses.

But an unrealised loss is still a loss.

On your books, the value of your account is lower. If you were to liquidate everything, you’d be down that amount. Thinking an unrealised loss is “not real” is a dangerous delusion that leads to poor decisions.

Don’t let unrealised losses be a reason to accept whatever risk the market gives you. Fight like hell to keep your risk exposure where you want it to be (with consideration to the cost of rebalancing, of course). It’s one of the only things you have any control over.

The Bigger Lesson

The broader lesson here is that rebalancing to a risk target isn’t primarily about maximising returns (although often that’s a nice side effect). It’s doing a specific job: keeping your risk exposure under control.

It’s always tempting to do the thing that maximises returns in the backtest. But in the case of rebalancing a volatile position, that’s making two mistakes:

Thinking rebalancing is about maximising returns. It’s not. It’s about keeping your risk exposure where you want it.

Thinking your backtest is the thing to optimise for. Your backtest is a guide, not a gospel. Use it to understand implementation trade-offs and get a sense of historical performance. Don’t optimise for it.

Rebalancing is about staying in control. In a trade this volatile, that matters more than squeezing out a few extra points of return.

Interesting strategy! Still need a strong stomach to trade the “widow maker”!