Have Edge, Will Travel

The cheapest diversification in trading is an edge you already have

For the solo trader, diversification largely comes down to finding more things to trade. But finding new things from scratch is only one way to get there.

There’s a cheaper route, too. Take an edge you already have, one you understand and trust, and port it somewhere new.

You already understand the underlying mechanism and have an implementation that works. The only question is whether it applies in other places, too. When it does, you actually get more than two things for the price of one. More on that shortly. First, why it’s the cheaper option.

The hard yards in trading don’t go into placing the trade. They go into finding something that works and, more to the point, working out why it works. The why is what tells you whether you’ve found a real edge or just a pattern that happened to fit the recent past.

Once you’ve paid for that understanding, you’re sitting on an asset. You’ve got a reason that something works, but you’ve only ever pointed it at one market. The reason doesn’t know it’s only allowed to work in US large caps. If it’s real, and if it’s driven by something structural, there’s a fair chance it turns up wherever that same structure exists.

This begets a simple question every time you’ve got an edge you trust: Where else might this same mechanism hold?

Let me show you a couple of things from our recent research. One worked. One didn’t. Both reveal useful things.

Case one (the one that worked)

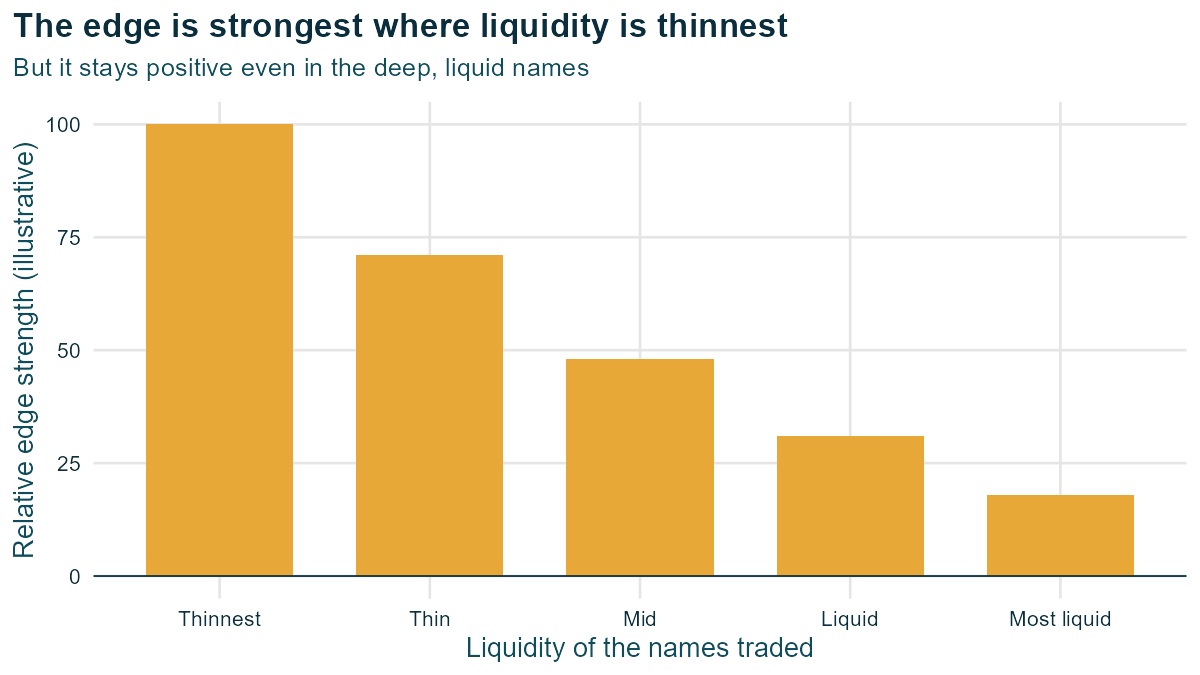

One of the strategies we trade makes its money by providing liquidity to short-term, flow-driven moves in stocks. Somebody comes in and pushes price around for reasons unrelated to what the company is worth, and we take the other side and collect as it settles back. That’s the whole edge, more or less. We know why it’s there and why it sticks around.

The edge does the most for us in the thinner, less-liquid names. When something illiquid gets pushed, it moves further, so there’s more to fade (the trade-off is that you can’t get as much size into it as you might like). The version of the strategy we already run leans into those names (within reason; we’re not total maniacs), where the effect is strongest.

So we asked the simple question. Does the same edge still pay if we point it at the bigger, more liquid names too?

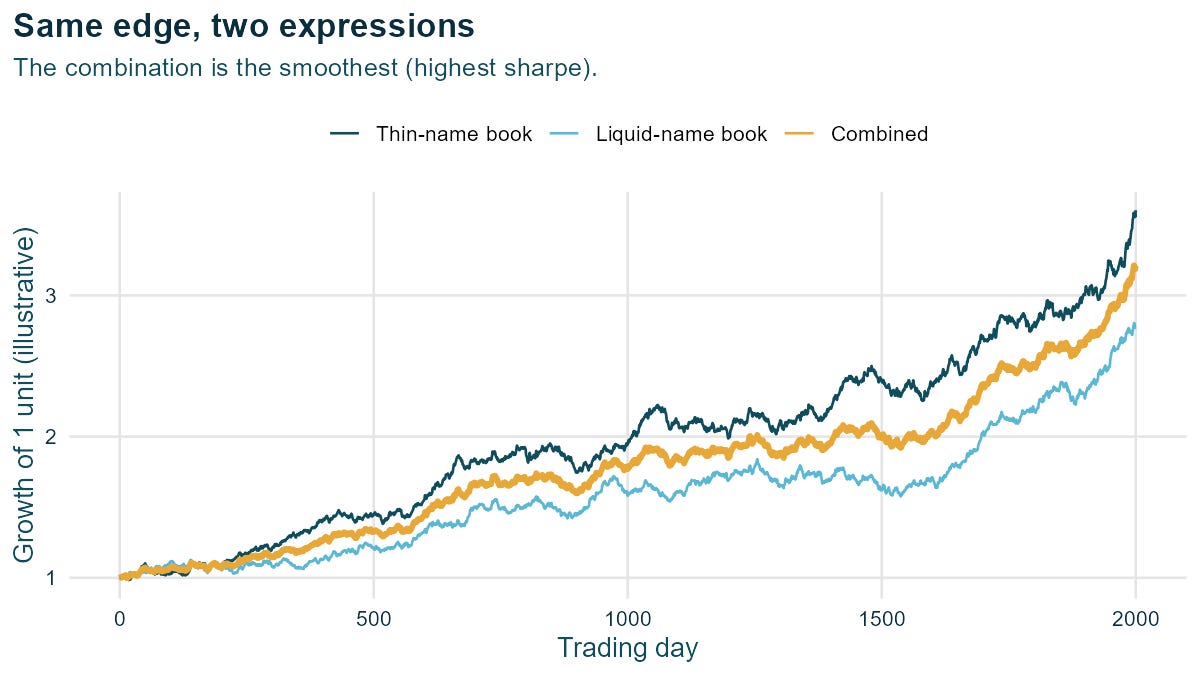

It does. Less, but it does. In a deep, liquid stock, the same flow barely nudges the price, so there’s not as much to fade, and the edge is weaker. But it’s still solidly positive. And, crucially, in this case it has much higher capacity.

And it’s worth the bother because those higher-quality names are a set we weren’t really trading before, and they move differently from the thin ones. So we get a second book of positions out of an edge we already had, with nothing new to discover.

You might wonder why we weren’t trading those names all along. We were, in the sense that they were always in front of us. They just sat on the bench. We make more in the thin names, so that’s where the book concentrated. But we’re now approaching capacity in those names. Pulling the liquid names into a second book, via a more aggressive set of filters, is a deliberate call: a weaker slice of the same edge, traded for a fresh set of positions that don’t move in lockstep with the first lot.

You might think running one edge in two places just gives you more of the same thing. Sometimes it does. But not here. The positions are different, and they get pushed around by different flows on different days, so the bumps don’t line up. It’s the same edge underneath, but the day-to-day ride is its own thing, and that difference is where the diversification comes from.

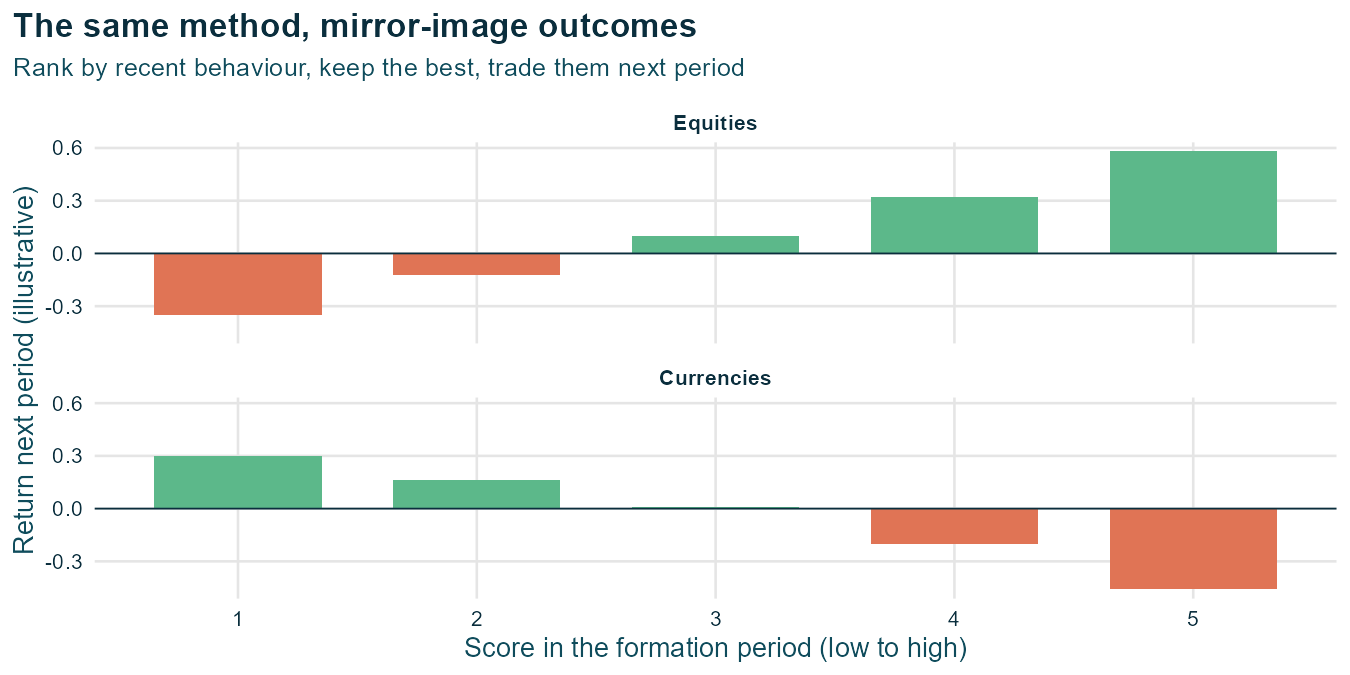

Case two (the one that fell flat)

Around the same time, we tried to take a method that works a treat in stocks and apply it to currencies. The method is simple enough: rank the things that have been behaving the way you want, keep the best ones, trade those next month. In stocks, it works, and it works well.

In currencies, it did the opposite. The ones that scored best went on to do the reverse of what we were after.

I don’t fully know why. Something about the way currencies move that doesn’t show up in stocks. But that’s not really the point. The point is we found out for the price of an afternoon, kept the bit that worked, and binned the bit that didn’t. A redeployment that fails costs you almost nothing and teaches you something about both markets. That’s a good trade on its own.

Redeploying an edge is cheap, but it isn’t automatic. You shouldn’t assume the reason it works exists in the second market. The same mechanism-first rigour you used the first time has to apply in the new market.

The good news is it’s a far easier job the second time around. You already know what you’re looking for. You start with a hypothesis (this should work over there too, for the same underlying reason), and you test whether that reason actually holds in the new place. The same simple data analysis techniques that helped you understand the edge in the first place can be reused here. But don’t jump straight to the backtest.

A successful transfer of an edge to a new market is worth more than double.

The payoff comes in two parts. The first is more confidence in the edge itself.

A very useful question when doing edge research is “does this effect show up in other places I expect it to, given my hypothesis for the mechanism?”

If something works in a new place for the same underlying reason, that’s a point in favour of the edge being real rather than a statistical quirk. You’ve run an out-of-sample test that no amount of fiddling with your original backtest could give you.

The second payoff is the new way to trade it. A fresh expression of an edge you already trust, ready to stack alongside the original.

The classic example here is momentum. The tendency of winners to keep winning, for a while, turns up in individual stocks, in country equity indices, in bonds, in commodities. It’s been documented across all of them. Carry, getting paid to hold the higher-yielding thing, is the same story across many of the same asset classes.

That ubiquity is doing two things at once. It’s a part of why researchers actually believe these edges are real, because a fluke doesn’t show up across unrelated market after market for the same structural reason. And it’s why a portfolio that harvests momentum or carry everywhere at once gives a smoother ride than doing it in a single place.

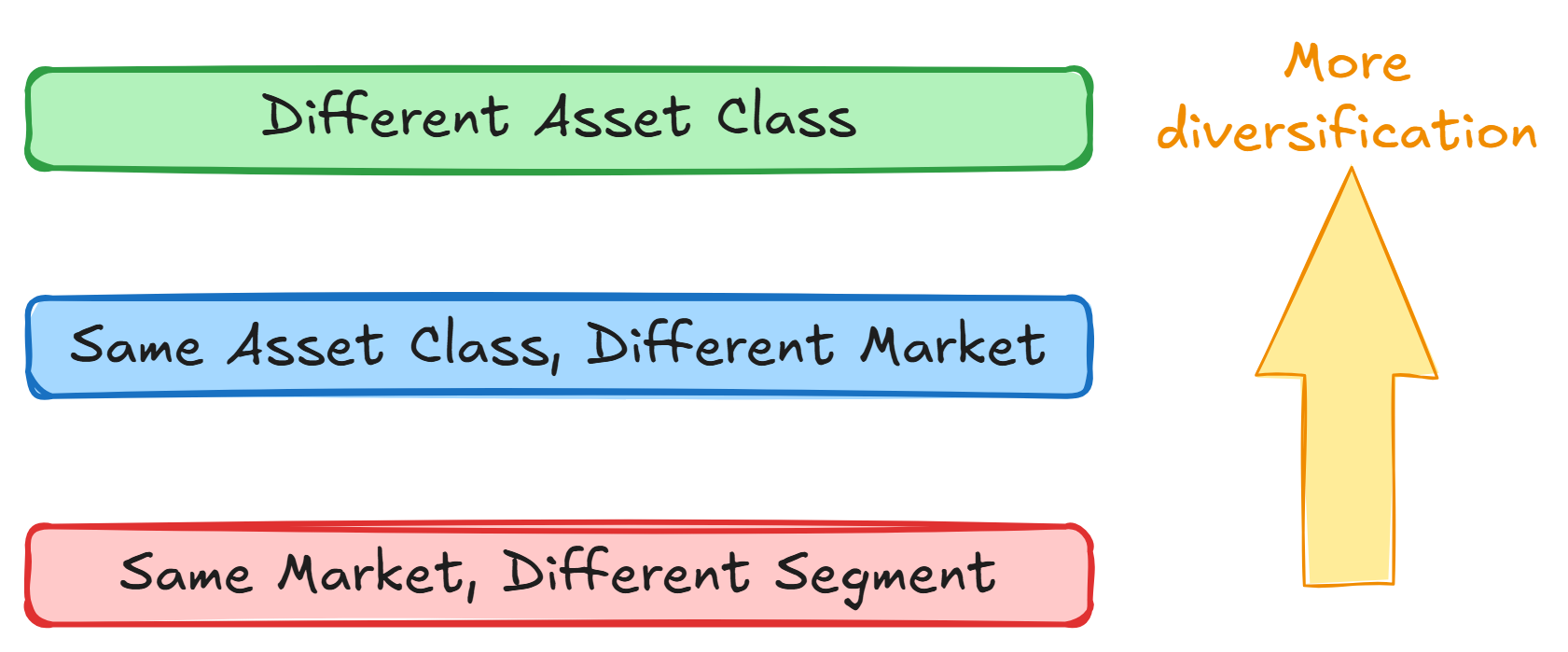

Earlier I said a second expression sometimes barely helps. Sometimes redeploying an edge gives you a lot of diversification, and sometimes it gives you next to nothing. It depends on how differently the edge shows up and how different those markets really are.

Run the same trade at the long end and the short end of the government bond curve and you’ve barely diversified at all. Ten-year and thirty-year yields are mostly joined at the hip. You’ve doubled the positions but barely changed the risk.

Take a market-neutral equity approach you trust and run it in another country’s market, and you’ve done better. Different companies, different flows. But both books will still tend to have their worst days at the same time. You’ve diversified the ordinary days and kept most of the tail.

Carry that same approach across to a different asset class altogether, and the diversification takes another step up. What hurts a market-neutral equity book needn’t hurt a commodities one. The ordinary days are uncorrelated, and a lot of the bad days are too.

None of this means the higher rungs are always better. An edge you understand deeply in equities might not have any natural analogue in commodities, and forcing it there to chase the diversification is how you end up trading a backtest. So don’t assume - think about the mechanism and go looking for evidence in the data.

You can do a version of this on whatever you trade, this week, without any fancy kit.

Pick one edge you trade.

Write down why it works, in plain words. The structural reason. Who’s on the other side, and why they keep showing up. If you can’t write it down, that’s your first job, and it’s worth doing regardless.

List the places that same reason might also hold. A different corner of the same market, a different market in the same asset class, a different asset class entirely, even a different time horizon. Don’t filter yet, just list.

Test each one properly. Same rigour as the original.

Keep what transfers, and note how correlated it is to the original. The less it moves in lockstep, the more it’s worth to you.

You won’t be right every time. We weren’t. But each test is cheap, and the ones that land cost you almost nothing extra to find.

The most valuable edge you’ve got might be one you’re underusing. You’ve already done the hard work of finding something that works and understanding why it pays. Asking where else that same reason holds is the cheapest research you’ll ever do, and when it pays off, it gives you two things at once: more reason to believe the edge, and another way to trade it.