Crypto Crash Post-Mortem

ADL, platform risk and what I'd do differently

It’s just over a week since the crypto flash crash.

If you got caught up in it, I’m genuinely sorry. It sucked. There wasn’t a whole lot you could have done to sidestep it - it wasn’t specific to a platform, a chain, or even a particular coin. The only way you really avoided it was by being out of crypto entirely.

Systematic trading is about showing up, doing the hard work of grinding out our edges over time, and doing the best we can with what we know.

In the spirit of fleshing out “what we know,” let’s talk about what happened, what it means, and what I learned.

The Uncomfortable Truth About Auto-Deleveraging

The crypto ecosystem is basically thousands of live experiments in economics, finance, and technology running simultaneously. Most of these experiments fail spectacularly. A few lead to genuine breakthroughs. All of them have unintended consequences and different sets of trade-offs.

This is both crypto’s greatest strength and its most dangerous liability.

The edge cases - the moments when everything goes sideways - are where these experiments get truly tested. It’s where you find out whether someone’s clever idea actually works under stress, or whether it just shifts risk around in ways that seemed fine until they very much weren’t.

Saturday was one of those moments.

One of the more interesting experiments in crypto has been around counterparty risk management.

Traditional exchanges solved this problem decades ago with clearing houses, insurance funds, and standardised margin requirements. Crypto is an opportunity to run a bunch of different experiments to see if there are better ways that can work under different use cases.

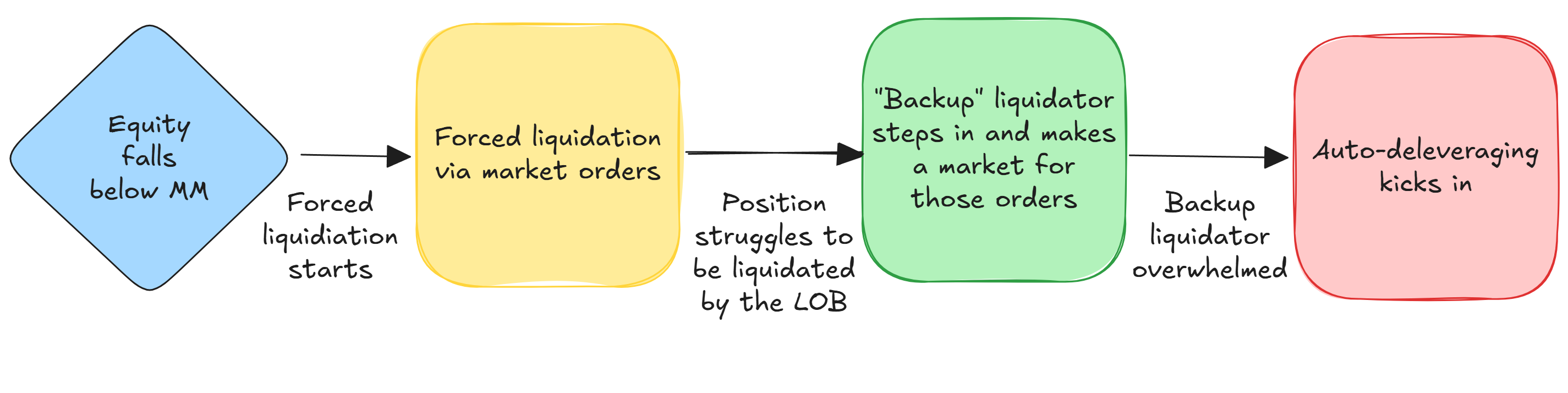

Auto-deleveraging (ADL) is one of those experiments.

ADL is a philosophical design choice that prioritises platform solvency over winning traders keeping all their profits.

It feels deeply unfair when you’re on the receiving end of it. You were in the right positions. The market moved in your favour. And then suddenly you’re forced to exit at worse prices because someone else blew up their account.

But there’s a trade-off: that mechanism is precisely what kept Hyperliquid (and other platforms) from accruing bad debt and potentially going under.

Different exchanges handle this differently. Some have insurance funds that absorb bad debt until they run out. Some socialise losses across all users. Some use ADL to force profitable traders to close out losing positions. Many use a combination.

There’s no perfect solution - only different sets of trade-offs.

The key is understanding the trade-offs for the platforms you trade on and deciding whether you’re comfortable with them.

What I Got Wrong

I’ve been trading on Hyperliquid for several months now. I’ll be honest - before last weekend, I didn’t fully understand the details of Hyperliquid’s ADL system. I knew it existed, but I hadn’t dug into the specifics.

That was lazy of me. I’ve now fixed it. You should do the same, if you haven’t already.

Go read the documentation for whatever platform you’re trading on. Understand the waterfall of liquidation mechanisms:

How does standard liquidation work?

What happens if that fails?

Is there an insurance fund or backup liquidator?

When does ADL kick in, and how are users selected?

If your platform doesn’t use ADL, what does it do in these “last resort” situations?

This isn’t exciting work, but it’s important. These edge cases matter precisely because they happen at the worst possible time - when everything’s already going pear-shaped.

I was running a reasonably sensible 2.5x leverage on my positions. Had plenty of buffer to my maintenance margin. Didn’t matter. I still got ADL’d because of what was happening to the system as a whole. Careful position sizing can’t protect you from the system-wide risk that contributed to this.

That’s worth thinking about. Is it a risk you want to take? If so, how big do you play the game?

The Feedback Loop

What made Saturday so brutal wasn’t just the initial selling. It was the feedback loop of liquidity destruction.

Here’s how it played out:

Initial heavy selling comes in during a quiet market period

Market makers pull quotes and widen spreads (sensible risk management on their part)

Now there’s less liquidity to absorb the selling, so prices move further than they otherwise would

Those bigger moves trigger more liquidations

Liquidations mean more forced selling

Which triggers more quote pulling, more liquidations, bigger moves...

And on and on until it stabilises.

The TradFi Alternative Worth Considering

Here’s something I’ve been thinking about: if you’re just trading the big four (BTC, ETH, SOL, XRP), you can do that on CME.

I run a simple multi-factor model on the top ten crypto assets by market cap. I was actually surprised to find that the backtest is pretty solid using just those four available on traditional exchanges.

Running a version of that strategy using a four-asset universe on CME essentially trades systemic platform risk for concentration risk. That might be a decent trade-off.

Yeah, there are still risks. Your broker could get into trouble, for instance. But the Russian doll of potential failure points is much smaller. You don’t face the same systemic risks on a traditional exchange as you do on crypto platforms. Let’s be honest… It’s still the wild west, and will be for some time.

Something to think about.

What I Would Have Done Differently (And Why It Matters)

This is the interesting bit: what I would have done differently would have actually cost me money this time, but I still think it’s the right approach.

I’m running a roughly delta-neutral, multi-factor long/short strategy. Classic quant trading approach.

If I’d been at the screen when this was happening, I would have cut my long positions as soon as I realised I was getting ADL’d on the shorts.

At that moment, I would have had no idea what was going to happen next. The market could have kept tanking. I would have been sitting there net long with no edge whatsoever.

I got lucky. The market came back. But counting on that is not how you build a sustainable trading business.

The fundamental principle here is this: I only want exposure where I have an edge.

The moment I got ADL’d, I had zero edge in predicting what would happen next. The right move would have been to balance my exposure as best I could, even though this time it would have cost me profits.

This is the meta-lesson: always keep in front of your mind what you actually have an edge in.

Trading is hard enough when I do have an edge. I don’t want exposure to situations where I don’t have one.

What It Means for Crypto Going Forward

We’re going to lose a chunk of users, at least temporarily. Whether it’s true or not in this specific case, there’s a perception of manipulation and no real recourse when things go wrong.

That perception isn’t going to be helped by events like this.

Maybe this erodes certain edges.

The carry trade and basis opportunities depend a lot on FOMO-driven speculative trading. If that user base shrinks permanently, those opportunities might diminish too.

Then again, maybe it doesn’t. People will probably eventually come back, if history is a guide.

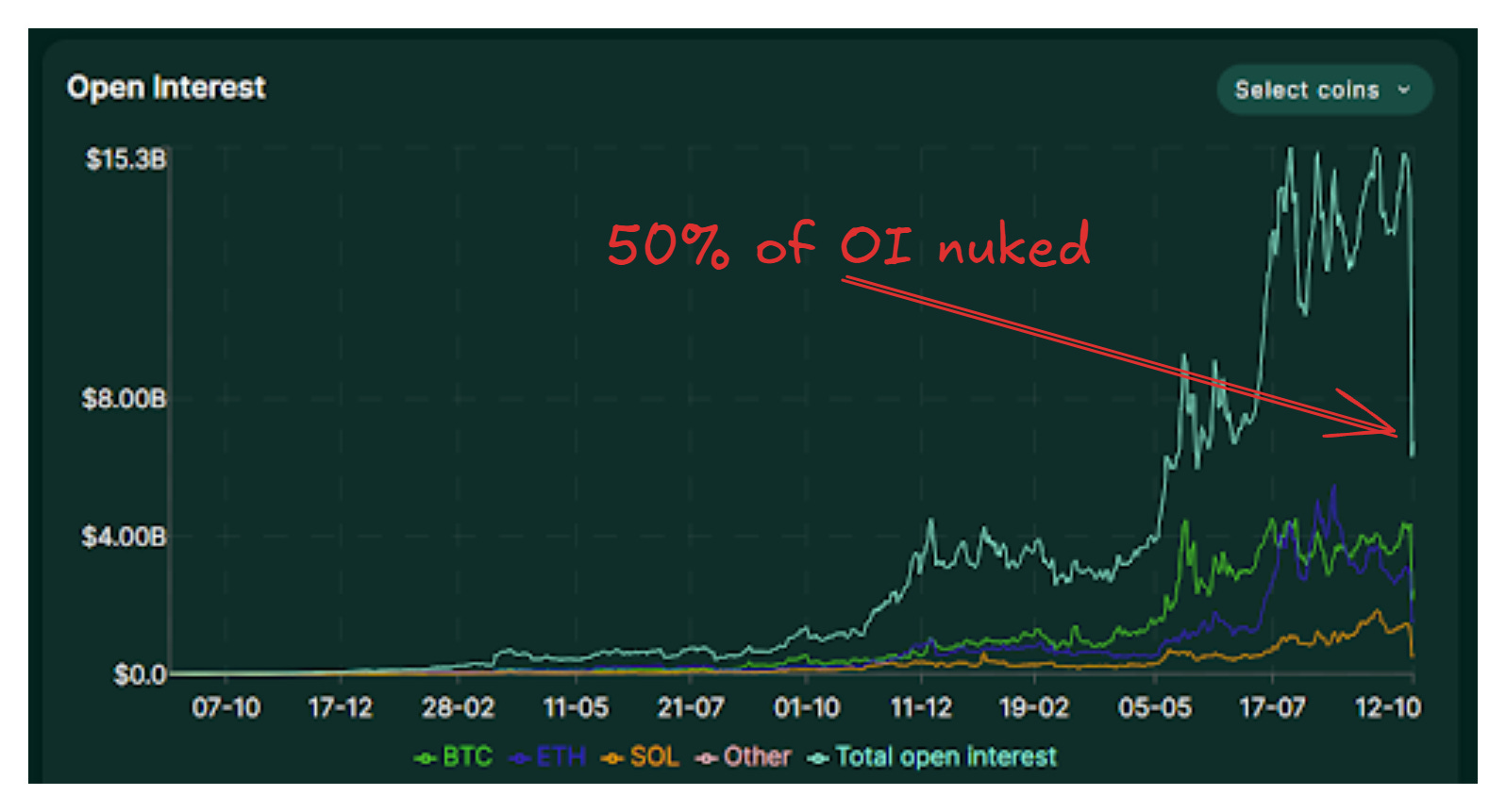

I’m not changing my approach for now. Still running my strategies, just with a slightly smaller size given the increased volatility. But I’m watching OI and funding rates with interest.

The Only Wrong Answer

I’m not going to tell you whether you should or shouldn’t trade crypto. That’s deeply personal and depends on your risk appetite, your goals, your constraints, and your stage of life.

Both of these statements are correct:

“I accept the risks with eyes wide open because the potential opportunities justify it for me.”

“For me, the risk of losing everything I put in just isn’t worth those potential opportunities.”

The only wrong approach is not thinking about it in terms of trade-offs.

The opportunity in crypto is real. You can run strategies that worked in traditional markets twenty years ago, and they still work today. That edge exists because of natural constraints on institutional players combined with a large retail user base doing FOMO and noise trading.

The risks are also enormous. Everything can go to zero. Not just because it becomes worthless, but because of scams, manipulation, and financial engineering experiments gone awry.

For me, I never had more than a chunk of my trading capital in crypto. If I’d lost it all on Saturday, it would have made me quite sad, but it wouldn’t have been catastrophic. That’s the right calculus for me.

Yours might be different. And that’s completely fine.

What Now?

Here’s what I’m doing:

Immediate actions:

Actually understanding the liquidation mechanics of every platform I trade on (should have done this ages ago)

Considering moving some core positions to CME to reduce platform risk

Setting up alerts for liquidation events so I know immediately if ADL happens

Maintaining proper position sizing where I can afford to lose what I have in crypto

Watching closely:

Open interest levels. Are traders coming back?

Funding rates. Is the speculative interest returning?

Whether the edges we’ve been trading are still there with a smaller user base

Not changing:

The fundamental approach of grinding out small edges over time

The principle of only taking exposure where I have an edge

Position sizing discipline

The game hasn’t fundamentally changed. We still show up, grind out our edges, and manage risk as best we can.

But last weekend was a good reminder that crypto carries risks that just don’t exist in traditional markets, and we need to factor that into everything we do.

What’s your take on ADL versus insurance funds versus socialised losses? Genuinely interested in hearing different perspectives on this. What trade-offs matter most to you?

Drop a comment or hit reply. I’d love to hear your thoughts.